Disclaimer: By providing links to other websites, A New Day - A New Earth does not guarantee, approve or endorse the information or products available on those websites.

The False Flag That Set the Stage

Predictive Programming - Programming the Subconscious for the Sinking of the Titanic

Predictive programming is the art of psychological conditioning of the subconscious by showing images of future events in books and movies so those events will be accepted as 'natural' when they actually occur and will not be resisted.

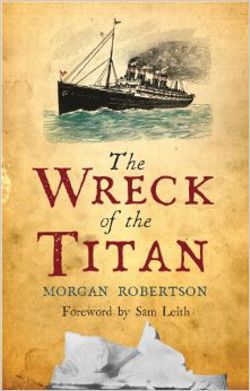

It's the story of the world's largest luxury liner called the Titan. It was called 'unsinkable' and it took it's maiden voyage in April.

It was going too fast in the North Atlantic Ocean when it hit an iceberg killing more than half of the 2,500 people onboard. There were only 24 lifeboats for the 2,500 passengers.

Sound familiar?

The author died of poisoning

Morgan Robertson, the author of The Wreck of the Titan, died of poisoning two years after the sinking of the Titanic.

Comparing the Titan and the Titanic

The fictional Titan and the Titanic were both considered the 'world's largest luxury liners' and 'unsinkable'.

The Titan was 244 meters long; the Titanic was 269 meters long.

Both made their maiden voyages in April in the North Atlantic Ocean.

They both had a passenger capacity of 3,000 people, with the Titan have 2,500 people onboard during his voyage and the Titanic having 2,300.

Both vessels had the minimum number of lifeboats - the Titan had 24 and the Titanic had 20.

Both vessels sank after hitting an iceberg in the North Atlantic Ocean and both were 644 kilometers from Newfoundland at the time.

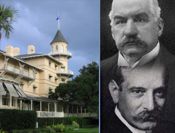

FACT: Jacob Astor, the richest man in the world at the time, Benjamin Guggenheim, after whom the Guggenheim Museum in New York City is named, and Isa Strauss, with a combined wealth that today would be more than US$11 billion. ALL OPPOSED THE FORMATION OF THE FEDERAL RESERVE BOARD.

FACT: They were all aboard the Titanic and died at sea, thus eliminating the strongest opposition to the formation of the Federal Reserve System.

Same Families That Set Up And Control The Federal Reserve Now Control The BIS And All But Three Central Banks

The same eight families that set up and control The Federal Reserve System of the United States (see left above), set up the Bank of International Settlements (BIS) in 1930 Basel, Switzerland. They gained control of all but three of the central banks of the world. The three central banks they do not control are the central banks of Cuba, Iran and North Korea.

The Rothschild family is believed to have the controlling interest in the BIS and the world's central banks.

"The powers of financial capitalism had another far-reaching aim, no less than to create a world system of financial control in private hands, able to dominate the political system of each country and the economy of the world as a whole.

"This system was to be controlled in a feudalist fashion by the central banks of the world acting in concert, by secret agreements arrived at in private meetings and conferences.

"The apex of the system was to be in the Bank of International Settlements in Basel, Switzerland, a private bank owned and controlled by the world's central banks - which were themselves private corporations." (pp. 324~325)

Links:

The Federal Reserve Cartel, by Dean Henderson. A brief history of the eight families control the world's central banks and most of the planet's resources.

The Federal Reserve is a Private Corporation

Federal Reserve System, Marriner Eccles Building, Washington, D.C.

The "Federal Reserve System" is neither 'federal' - it is not a public entity - nor does it have any 'reserves'. It is a private corporation controlled by non-Americans.

The Secret 1910 Meeting on Jekyll Island

In the fall of 1910, a group of six men secretly met on Jekyll Island off the coast of Georgia. Only first names were used.

They represented the banking dynasties of the Rockefellers, J.P. Morgan, Paul Warburg and the Rothschilds.

They met for the purpose of developing a plan to establish a privately owned central banking system for the United States.

their approval, they called the private corporation the 'Federal Reserve'. (See links below for historical details.)

Woodrow Wilson Signs Law Establishing The Federal Reserve in 1913

With the major opposition to the establishment of the Federal Reserve law removed with the sinking of the Titanic, Woodrow Wilson, whose campaign for the U.S. Presidency was financed by J.P. Morgan, signed the law establishing The Federal Reserve two days before Christmas on Dec. 23, 1913, when most lawmakers had already left Washington, D.C. for the holidays.

Powers of The Federal Reserve

The Federal Reserve Act in 1913 set up The Federal Reserve System and gave it the power over the money supply for the United States. It could decide how much money to print and put into circulation and require the United States government to pay the Federal Reserve interest on the money.

Thus, the U.S. immediately has a debt as soon as the money printed by The Federal Reserve is put into circulation. In other words, money is created out of debt - owed by American taxpayers.

Who Owns The Federal Reserve?

The Federal Reserve Bank of New York, by far the most important of the 12 member banks, was dominated by the Rothschilds of London and Paris and seven other families: Goldman Sachs, Rockefellers, Lehmans and Kuhn Loebs of New York, the Warburgs of Hamburg, the Lazards of Paris and the Israel Moses Seifs of Rome.

The Rothschilds, Rockefellers, Kuhn Loebs and Warburgs are four of the 13 bloodline families of the Illuminati.

It is believed that 9 banks originally controlled the 12 branches of the Federal Reserve Board System:

* N.M. Rothschild of London

* Rothschild Bank of Berlin

* Warburg Bank of Hamburg, Germany

* Warburg Bank of Amsterdam

* Lazard Brothers of Paris

* Kuhn Loeb Bank of New York

* Israel Moses Seif Bank of Italy

* Goldman Sachs of New York

* J.P. Morgan Chase of New York

Who Received The US$27 Trillion Bailout after the 2008 Financial Crisis?

The same banks that own the Federal Reserve received the US$27 trillion bailout after the 2008 financial crisis.

The Federal Reserve Cartel, by Dean Henderson. A brief history of the eight families control the world's central banks and most of the planet's resources.

"Zeitgeist Addendum" - a documentary on The Federal Reserve System and Fractional Reserve Banking

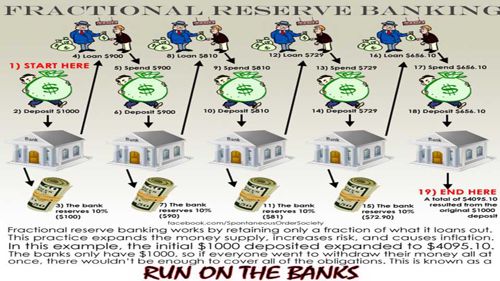

Fractional Reserve Banking -

How the Banks Create Money Out of Thin Air

Do you know that when you deposit US$1,000 cash in a bank, the bank is allowed to lend out US$900 to someone else and keep US$!00 on reserve. The person who received the loan of US$900 can buy something with the money and the seller will deposit the US$900 in a bank. That bank can lend US$810 of that US$900 deposit to someone and keep US$90 as a reserve.

This process can continue until the original US$1,000 deposit has generated US$9,000 of money on the books for the banks involved. This is creating money "out of thin air" and it is called Fractional Reserve Banking.

One Problem with Fractional Reserve Banking - Bank Runs

Since the banks only keep 10% of the deposits they receive in the form of a cash reserve, they could quickly experience a liquidity crisis if many depositors desired to withdraw their money at the same time. This is called a run on the banks.

Today, the U.S. banking sector has deposits totaling more than US$10 trillion, but cash reserves of around US$1 trillion. This is one reason the bankers are trying to eliminate cash, and, thus, force depositors to only use banks to store their money.

"Hitler Was Financed by the Federal Reserve and the Bank of England" - Yuri Rubtsov, PhD History

Veterans Today published an English translation of an article by Yuri Rubtsov, which was originally published in 2009 at ru-polit.livejournal. Rubtsov has a doctorate in history and is a professor at the Military University, Russian Ministry of Defense.

Dr. Rubtsov describes a four-stage plan from 1919 to 1939 by the Federal Reserve, the Bank of England, and various American industrialists to gain absolute control of the financial system of Germany and thereby control Central Europe.

This was done in part by financing the efforts of Adolph Hitler and his rise to power.

The article and the documentary films below describe the Cabal's use of the Babylonian Money-Magic System to create wars by financing both sides of conflicts and using such financing to control countries' financial and political systems.

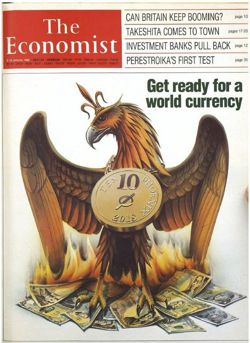

The January 1988 issue of "The Economist" magazine, controlled by the Rothschild empire, had a phoenix standing above burning currencies from around the world, including the U.S. dollar, the Japanese yen and the Chinese yuan.

Around the neck of the phoenix was a gold medallion with the inscription: "10 Phoenix 2018" and next to the phoenix was the title of the cover story: "Get ready for a world currency".

"THIRTY years from now, Americans, Japanese, Europeans, and people in many other rich countries, and some relatively poor ones will probably be paying for their shopping with the same currency.

"Prices will be quoted not in dollars, yen or D-marks but in, let's say, the phoenix. The phoenix will be favored by companies and shoppers because it will be more convenient than today's national currencies, which by then will seem a quaint cause of much disruption to economic life in the last twentieth century.

This Was Predictive Programming To Set The Stage For A One World Currency And A One World Government

How could the Cabal/Illuminati achieve their goal? As we are now experiencing, they could achieve their goal by weakening the economies, societies and governments of the strongest parts of the world - the United States and Europe.

What's the Primary Stated Reason for Banning Cash?

The primary stated reason for banning cash is to make it harder for criminals to commit crimes and launder money.

What's the REAL Reason for Banning Cash?

The REAL reason for banning cash is to prevent depositors from withdrawing their money from banks due to a loss of confidence in the banking system. This loss of confidence could be due to negative interest rates - you have to pay the banks to keep your money in the banks - or a meltdown of the financial system.

In the Case of a Bank Failure, the Bank Can Legally KeepYour Deposit In Some Countries, Including the U.S. This Is Called a Bail-In.

This is known as a 'bail-in' and was authorized by a number of countries, including the U.S. after the 2008 Financial Crisis. It was sold by telling people that as taxpayers they would not have to bail-out the banks in the next crash. What they didn't tell people was that they would still have to pay by losing a portion of, or all of, their bank deposits.

Fiat money is actually not money. It is paper printed by a government which declares by law that it is 'legal tender' and can be used to pay for goods and services. Fiat money is backed by the trust people have in the government that issued the paper currency.

Asset-backed currency is money issued by a government that is backed by some asset like gold or silver.

Before 1933, U.S. currency was backed by silver. If you had a $1 bill, called a Silver Certificate (notice 'Silver Certificate' at the top), you could take it to a bank and exchange it for one silver dollar. (Notice at the bottom: ONE SILVER DOLLLAR PAYABLE TO THE BEARER ON DEMAND.)

In 1933, the U.S. stopped issuing silver certificates and began to issue Federal Reserve Notes (notice 'Federal Reserve Note' at the top). 'One Silver Dollar' was replaced with 'One Dollar'. Near the top left was added: 'This note is legal tender for all debts, public and private.'

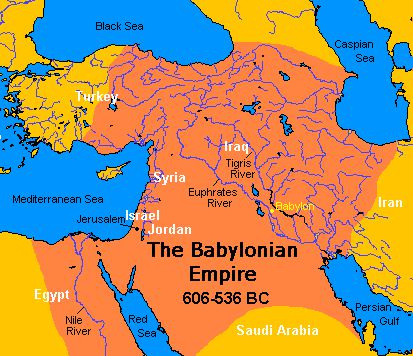

Capitalism started in Babylon, the present day Iraq, around 2,000 B.C.

The rulers discovered that they could lend money to kingdoms to fight wars and end up controlling the kingdoms as debt-slaves.

The kingdoms that borrowed the money then had a debt. If they didn't repay the debt, they were taken over.

So the rulers of Babylon were the first to recognize that those who controlled the money supply also controlled governments and people by issuing debt.

Established to Protect Pilgrims Visiting The Holy Land

Webb and his sources explain that the Knights Templar, which were originally formed in 1119 with nine knights by a French nobleman, were formally organized as the Knights of the Temple of Soloman of Jerusalem in 1129 and served to protect pilgrims from Europe wishing to visit the Holy Land.

Accumulate Vast Wealth

As the knights took various vows, including the vow of poverty, they acquired the land, money and other assets of those noblemen and knights who joined them and became "one of the richest entities in the world over just a few years, and with well established banks within their monasteries, and arguably the best security in the world for those assets."

Network of Over 9,000 Manors

In time, the Knights Templar accumulated and administered over 9,000 manors that had been given to them by pious benefactors. These manors and the Orders monasteries were administered by banker monks who looked after the Order's assets as well as assets stored with them by pilgrims, nobles and royal families.

First Safe Deposit Boxes

The Knights Templar were the first to introduce small safe deposit boxes for travelers, nobles and royal families.

People could leave their valuables in the boxes, which were inside monastery walls and protected by the Knights, and remove or deposit their valuables whenever they wanted.

Loans

The Knights also initiated issuing loans of their accumulated wealth and truly became bankers.

They were not the first to make loans, of course, but did so with a much larger network and better recordkeeping than had been done previously.

Templars were able to move wealth from location to location.

First Travelers Checks

"With such a trustworthy reputation established, the Templars issued a note to a person for the amount deposited in one place that was good for the person to collect such amount from the Templars in another place or region.

"The Templars were effectively issuing travelers checks to people upon deposit of monies. This was of great benefit to people traveling abroad and specifically to the Holy Lands where bandits and robbers made their livelihoods."

Pope Clement V Dissolves the Knights Templar in 1314

A little over 200 years after they were formed, Pope Clement V dissolved the Knights Templar in 1314 to effectively curtail their power and allow the King of France to confiscate their wealth at a time when France and King Philip were in financial dire straits.

Early History of The Rothschild Family Banking Dynasty

As described in the section on the Khazarian Mafia on The Dark Energy page, the ancestors of the Rothschilds were Khazars. The Khazars had practiced a Turkic religion called Tengrism, but around 800 A.D. were forced by Russia and surrounding countries to adopt one of the major religions of the day: Christianity, Islam or Judaism. They chose Judaism.

Further conflict with Russia and surrounding countries forced the Khazars to leave their homeland and spread out into Europe.

German Khazarian/Ashkenazi Jew Adopts The Name of Rothschild

Mayer Amschel Bauer, born in Frankfurt, Germany in 1744 to a Khazarian/Ashkenazi Jew. His father ran a counting house and was a money exchanger.

Upon his father's death, he returned to Frankfurt from Hanover, where he had worked for a bank operated by the Oppenheimer family.

He took over his father's business and changed his name to Rothschild because he liked the red hexagram shield that hung on the front door of his father's business. In German, 'rot' is 'red' and 'schild' is 'shield'.

An acquaintance that Rothschild met while working at the bank, General von Estorff, was associated with one of the richest houses of Europe, Hesse-Hanau. While selling 'valuabletrinkets' and coins, Rothschild was able to get General von Estorff to

introduce him to a member of the house, Prince William IX, who allowed him to join his circle of associates and let him put a sign on his office stating: "M.A. Rothschild, by appointment court factor to his serene highness, Prince William of Hanau." Rothschild was then able to become a court Jew providing loans to members of the court and nobility.

Mayer Amschel Rothschild had five sons. The eldest, Amschel Mayer Rothschild, stayed in Germany to assist his father's business and the rest established banks in Austria, England, Italy and France.

SM von Rothschild, Vienna

The second son, Solomon Mayer von Rothschild, went to Austria and established SM von Rothschild Vienna.

NM Rothschild and Sons, London

The third son, Nathan Mayer Rothschild, went to London and established NM Rothschild and Sons.

CM de Rothschild, Rome

The fourth son, Carl Mayer von Rothschild, went to Rome and established CM de Rothschild.

de Rothschild Freres, Paris

And the fifth son, James Mayer von Rothschild, went to Paris and established de Rothschild Freres.

Famous Quotes:

"Let me issue and control a Nation's money and I care not who makes its laws". Amschel Mayer(Bauer) Rothschild, 1838

"The few who can understand the system will be either so interested in its profits, or so dependent on its favours, that there will be no opposition from that class, while, on the other hand, that great body of people, mentally incapable of comprehending the tremendous advantage that Capital derives from the system, will bear its burden without complaint and, perhaps, without even suspecting that the system is inimical to their interests." Stated in a letter from the Rothschilds of London to their New York agents in 1912 introducing their banking methods. (Source)

In 1835, Andrew Jackson was shot at by a man using two different handguns, but both misfired. He later told his Vice President, "The bank, Mr. Van Buren, is trying to kill me . . . "

Three years earlier, Jackson had vetoed the renewal of the charter of the Second Bank of the United States - a private bank with government powers controlled by the Rothschild family. It was a forerunner to today's Federal Reserve System.

Abraham Lincoln

In 1865, Abraam Lincoln was killed by John Wilkes Booth, a Rothschild agent. Lincoln had sought to prevent the Rothschild's from financing the Civil War. He knew that by doing that, the Rothschild's would control the U.S.

So Lincoln issued government bonds, called Greenbacks, to raise money from American citizens to fight the war.

James Garfield

James Garfield was shot and killed in 1881 after only four months in office. He had publicly stated that whoever controlled the supply of currency would control the business and activities of the people.

John F. Kennedy

JFK signed an order on June 4, 1963 to take the power of printing money away from the Federal Reserve System and give it back to the U.S. Government. He had new currency printed that was backed by silver, but he was shot and killed on November 22, 1963. The new administration of Lyndon Johnson removed the silver certificate from circulation and the Federal Reserve Notes continued to be the U.S. currency.

Financial Crisis of 2008 - A Planned Event

The Financial Crisis of 2008 was a planned crash by the Cabal. One purpose was to suck trillions of dollars out of the world economy. Another purpose was to further weaken the U.S. economy on the path toward a final 'solution' of a one world currency and one world government.

"The Warning", a 2009 PBS Documentary

For those who doubt this, please watch the 2009 PBS documentary, "The Warning", on the 2008 subprime loan crisis and the events leading up to it.

Catherine Austin Fitts

Also, watch the June 28, 2014 ProjectCamelot interview with Catherine Austin Fitts, a former Assistant Secretary of Housing/Federal Housing Commissioner of HUD (Housing and Urban Development) in the Reagan Administration. During the interview, Fitts explains about the 2008 financial crisis:

"So this was coming for the highest levels of the financial system – I mean government. This was a bubble engineered intentionally by government. They knew it was going to be fraudulent. . . .

we've gone through what I call a financial coup d'etat – a change of control. . . .

Well, here's the big question about where did the money go? . . .

[It] was about US$40 trillion that went some place. Now I think that some of it went into the emerging markets to balance the global economy. So you pull capital out of the mature economy and you reinvest it in the high-growth economy. . . . So some of it was rebalancing the global economy. But there was enough money left over to basically create a private endowment that could produce dividends and interest sufficient to run a world government without taxpayers." (Transcript PDF)

On July 1, 2005, the Chairman of then President George W. Bush’s Council of Economic Advisors told a reporter from CNBC that,

“We’ve never had a decline in house prices on a nationwide basis. So, what I think is more likely is that house prices will slow, maybe stabilize, might slow consumption spending a bit. I don’t think it’s gonna drive the economy too far from its full employment path, though.”

His name was Ben Bernanke. And within a year he would become Chairman of the Federal Reserve.

Of course, we know now that he was dead wrong.

The housing market crashed and dragged the US economy with it. And Bernanke spent his entire tenure as Fed chairman dealing with the consequences.

One of the chief culprits of this debacle was the collapse of the sub-prime bubble.

Banks had spent years making sweetheart home loans to just about anyone who wanted to borrow, including high risk ‘sub-prime’ borrowers who were often insolvent and had little prospect of honoring the terms of the loan.

When the bubble got into full swing, lending practices were so out of control that banks routinely offered no-money-down mortgages to subprime borrowers.

The deals got even sweeter, with banks making 102% and even 105% loans.

In other words, they would loan the entire purchase price of a home plus closing costs, and then kick in a little bit extra for the borrower to put in his/her pocket.

So basically, these subprime loan home buyers were getting paid to borrow money.

Of course we know how that turned out.

By 2008 the entire system crashed, and the post-game analysis had some pretty obvious conclusions:

Bad things tend to happen when you pay people to borrow money, especially when they're not particularly creditworthy.

Thank goodness no one in finance engages in such risky behavior anymore!

Or do they?

Today, subprime is back.

There’s been a lot of talk lately about a growing bubble in the subprime auto loan market, and even student loans.

But the biggest subprime bubble of all is the negative interest rate loans being made to sovereign governments.

All over the world now there are governments that are issuing sovereign bonds with negative yields… and many of these governments are totally bankrupt.

Japan, with its debt level at more than 220% of GDP, is the latest entrant into the world of negative interest bonds.

Japan’s debt is so high, in fact, that it takes 41% of government tax revenue to service.

Even in Italy, one of Europe’s most notoriously and hopelessly bankrupt countries, the government bonds have negative yields.

‘Negative yield’ means that an investor who loans money to government will get back less money than s/he invested once the bond matures.

In other words, the government is getting paid to borrow money.

So it’s not much different than when banks paid subprime homeowners to borrow money ten years ago based on a misguided premise that home prices always go up.

Now they’re just paying subprime governments to borrow based on a misguided premise that governments will ALWAYS pay. (Just like Greece!)

The key difference is size.

At the peak of the housing bubble ten years ago, there was about $1.3 trillion worth of subprime mortgages in the financial system.

That $1.3 trillion bubble was enough to bring down several major banks and cause cascading damage across the global financial system.

Today’s bubble is EIGHT TIMES the size of the last one, with more than $10.4 trillion worth of government bonds that yield negative interest.

And what’s even more concerning is how quickly it’s growing.

In January 2016, the total amount of government bonds in the world with negative interest totaled $5.5 trillion.

One month later in February the total had grown to $7 trillion. By May it was $9.9 trillion. And today it’s $10.4 trillion.

So this gigantic sovereign bond bubble where governments are being paid to borrow money has practically doubled just in the last several months.

This isn’t a cause for panic or to assume that the financial system is going to crash tomorrow. But it’s clearly a disturbing trend… the proverbial powder keg in search of a match.

And when future pundits write the history of the financial crisis to come, whether it happens today, tomorrow, or years from now, you can bet they’ll wonder how the entire system failed once again to see something so dangerous… and so obvious.

The Big Banks Have Rigged All Markets

In recent years, American and European banks have been convicted of or settled legal cases of rigging the following financial markets and continue to face lawsuits for market rigging:

"JP Morgan Chase was the subject of a criminal complaint. Now the complaint was not against the individuals who were responsible for this, but the bricks and mortar were charged with criminal violations of the Bank Secrecy Act, which is a felony violation. And JP Morgan Chase disgorged a small percentage of the profits it made on the Madoff relationship and the government called it quits. Nobody was fired. Nobody disgorged bonuses.

Greg Hunter: "The banks are criminal organizations. They're just all about making money by fraud."

Chaitman: "They are and they do it regularly - all of them. I could have written this book about HSBC or Bank of America or Citigroup. All of the banks - because the government has encouraged them to do this - all of the banks have been operating like criminal enterprises.

"Madoff had a group of people, a small group of people who were grossly over compensated, who would just make up the statements after the fact [for investor clients]. They never purchased a security. They had no stocks. They just had pieces of paper saying they had stocks."

"[Madoff] just kept all the money. And that's why JP Morgan liked him as a customer. He kept on deposit billions of dollars. And JP Morgan Chase was free to use that money for it's own purposes. . . .

"The bankers have become such criminals that it threatens the entire economy - the world economy. . .

"[The big banks] have admitted violating the foreign exchange rules. They've pled guilty to a felony in respect to that - to fixing the foreign exchange rate, which impacted millions of people. They've defrauded veterans. They've defrauded credit card holders. They've defrauded homeowners. There is no group of customers that they won't defraud if it can enhance their profits.

"And, yes, in the last four years alone, they have disgorged US$36 billion as settlements of charges brought with respect to all of these violations."

Is the Scale of Financial Fraud Larger than We Can Ever Imagine? Is the NSA Manipulating the Stock Market?

He first refers to a discovery in a December 2013 White House task force report by Trevor Timm of the Electronic Freedom Frontier. The task force was on 'spying and snooping' - NSA-type stuff.

WH Task Force Recommendations, #31, Section 2

Timm's discovery was this sentence under Recommendations, #31, Section 2:

“Governments should not use their offensive cyber capabilities to change the amounts held in financial accounts or otherwise manipulate financial systems.”

Then in a Tweet, Timm asked: "Does this NSA report recommendation imply that NSA is conducting offensive cyber attacks against financial systems?"

SPIEGEL Reveals NSA Widely Monitors International Payments

“The National Security Agency (NSA) widely monitors international payments, banking and credit card transactions, according to documents seen by SPIEGEL.”

“The NSA’s Tracfin data bank also contained data from the Brussels-based Society for Worldwide Interbank Financial Telecommunication (SWIFT), a network used by thousands of banks to send transaction information securely…the NSA spied on the organization on several levels, involving, among others, the [NSA] agency’s ‘tailored access operations’ division…”

NSA's 'Tailored Access Operations Division'

Rappoport indicates that, "The NSA's 'tailored access operations' division uses roughly 1000 hackers and analysts in its spying efforts."

He continues: "The next step in all this spying would naturally involve penetrating trading markets and, using the deep data obtained, manipulate the markets to the advantage of the NSA and preferred clients.

"The amount of money siphoned off in such an ongoing operation would be enormous.

“Looking over the shoulder” of Wall St. insiders would be child’s play for NSA."

Brad Thor's Novel About A Monster Corporation - ATS

Then Rappoport refers to a description of a monster corporation, ATS, in Brad Thor's novel "Black List":

“For years ATS had been using its technological superiority to conduct massive insider trading. Since the early 1980s, the company had spied on anyone and everyone in the financial world. They listened in on phone calls, intercepted faxes, and evolved right along with the technology, hacking internal computer networks and e-mail accounts. They created mountains of ‘black dollars’ for themselves, which they washed through various programs they were running under secret contract, far from the prying eyes of financial regulators.

“Those black dollars were invested into hard assets around the world, as well as in the stock market, through sham, offshore corporations. They also funneled the money into reams of promising R&D projects, which eventually would be turned around and sold to the Pentagon or the CIA.

“In short, ATS had created its own license to print money and had assured itself a place beyond examination or reproach.”

The Rise of the Meta-Criminal

Rappoport suggests that: "In real life, with the NSA heading up the show, the outcome would be the same."

And he concludes his blog post with this: ". . . we need to analyze what is happening in the world with a new dimension of criminal reality-maker in mind.

"New Confessions of an Economic Hit Man" by John Perkins

John Perkins was a Chief Economist for an international consulting firm for a number of years. The firm, which was basically an undercover operation of the U.S. intelligence agencies, advised the major global economic organizations - the IMF and the World Bank - as well as the United Nations, the U.S. Treasury Department and numerous Fortune 500 companies.

He would then seek to interest the leaders of developing countries in Asia, Latin American and Africa, in securing large loans for infrastructure projects which the countries would struggle to pay back and often be unable to pay back, thus, allowing global elites to seize the countries' assets and/or requiring that the countries' vote as told by global elites in international organizations, such as the UN.

The leaders of the developing countries were often bribed in order to get their countries to accept such loans. If the leaders refused, they would often become targets for removal from office or assassination.

After having a change of heart and escaping The Matrix, and in spite of being threatened and offered bribes to remain quiet, John wrote his first book, "Confessions of an Economic Hit Man" in 2004. It stayed on the New York Times non-fiction bestseller list for 73 weeks and has been translated into 32 languages.

yes! magazine published "The Debt Issue" in their Issue 75 Fall 2015 issue, and it is full of information on the mounting debt Americans find themselves in.

"The Debt Issue" includes an excellent infographic with startling information.

For instance, in 1980 the median household income was US$46,995. By 2012, 32 years later, it had increase by only 9% to US$51,371.

Yet, in that same 32 year period, the median price of a new home rose by 47%, the consumer price index rose by 250%, and expenses for medical services rose by a stunning 575%.

As the infographic headlines, Americans are "borrowing more for things income used to cover".

Debt in 2015:

The average auto loan in America was US$30,738.

The average credit card debt among indebted households was US$15,863.

The average student loan was US$33,090.

The average home mortgage balance was US$156,584.

Savings in 2015:

59% of Americans had less than US$500 in savings.

The average personal savings rate in 1980 was 10.5% and in 2015 it was 5.4%.

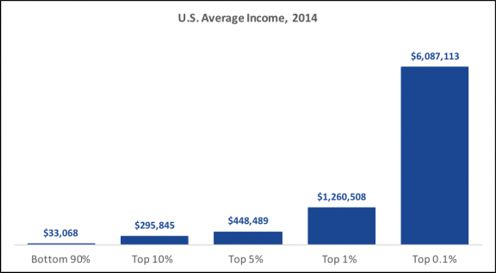

According to this chart, in 2014 the average income of a working American in the bottom 90% was US$33,068. For the top 10%, it was US$295,845. The average income for the top 0.1% of working Americans was US$6,087,113.

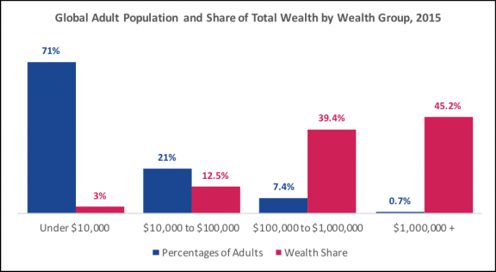

According to this chart, the bottom 71% of the global adult population share only 3% of the world's wealth. The top 0.7% share 45.2% of the world's wealth.

Links:

‘Income Inequality’. Published online at OurWorldInData.org. Retrieved from: https://ourworldindata.org/income-inequality/ [Online Resource]

Our World in Data - Data visualizations and empirical research that tell you how and why living conditions around the world are changing. A publication of Max Roser